Territorial tax law in Chile (law 17.235): history and calculation of property taxes

Territorial tax law in Chile (law 17.235): history and calculation of property taxes

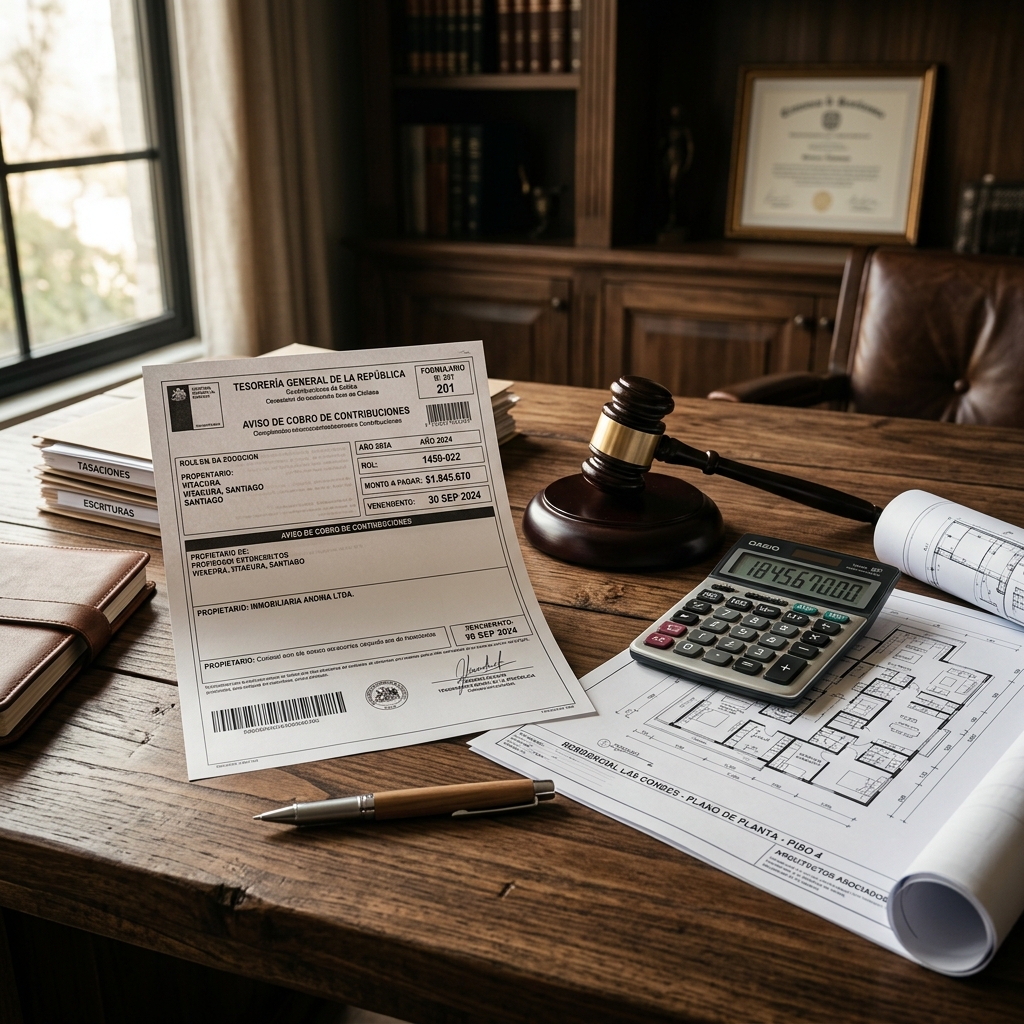

It is a scene that is inexorably repeated every quarter in thousands of Chilean homes. You open the mail and find the dreaded property tax collection notice, and the first reaction is confusion and helplessness at not understanding why the amount rises seemingly arbitrarily. You feel like you are paying an eternal rent for the house you already bought with your lifelong effort.

You should know that this collection is not a whim of the Internal Revenue Service, nor a random calculation performed behind closed doors. It is the strict and mathematical application of the territorial tax law, formally known as law number seventeen thousand two hundred and thirty five. This legislation establishes a rigid regulatory framework that forces the State to appraise and tax real estate property under specific technical criteria.

This article has been designed as the definitive technical guide for property owners to fully understand their tax obligations. Most importantly, we will break down your rights against the treasury, giving you the necessary legal tools to audit your charges, identify appraisal errors, and defend your real estate assets from unjustified tax burdens.

Origin and promulgation: the birth of law number 17.235

To understand how the current system works, it is vital to trace back to its genesis. The law was enacted and published in the Official Gazette at the end of the year nineteen sixty nine, during the government of President Eduardo Frei Montalva. Its original purpose was to systematize, modernize, and group into a single legal body the previously scattered regulations that governed the taxation of real estate in the country, creating a unified standard for fiscal appraisal.

Over the decades, this law has undergone constant evolution to adapt to the dynamics of the real estate market and the growth of cities. The consolidated and updated text that governs today was established by the decree with force of law number one of the year nineteen ninety eight, from the Ministry of Finance. Among its multiple modernizations, this standard established the fundamental classification of properties into two large tax series: the agricultural series and the non agricultural series, determining different treatments and rates for each.

The economic and social importance of the territorial tax

There is a widespread myth that the money collected from property taxes goes directly to the general coffers of the central government to finance ministries. This is completely false. The territorial tax is essentially a locally allocated tax, which means that one hundred percent of the proceeds are exclusively destined to finance the municipalities of Chile, being the economic engine that sustains the functioning of local governments.

The distribution mechanism is a key piece of social equity through the Municipal Common Fund. By law, a percentage of what is collected remains directly in the municipality where the property is located, guaranteeing resources for the maintenance of street lighting, cleaning, and green areas of your commune. The rest of the money is injected into this national solidarity fund, which redistributes revenues to finance the poorest and most vulnerable communes in Chile, making this law the main source of financing for urban and rural development at the national level.

Technical procedure: how the IRS determines the tax to pay

The process by which the Internal Revenue Service calculates how much you must pay is a highly regulated procedure that combines architectural appraisal and tax law. Everything starts with the fiscal appraisal. The service appraises your property strictly separating the value of the land on the one hand, and the value of the constructions on the other, using extensive tables of unit costs that analyze the quality of the materials, the age, and the destination of the property.

One of the main sources of confusion are the sudden increases in quotas. This is due to general reappraisals. By mandate of article three of the law, the treasury has the inalienable obligation to update the appraisals of all properties in the country every four years. This process seeks to capture and adjust fiscal values to the real capital gain of the market, reflecting the increase in land value due to new subway lines, paving, or commercial development in the sector.

It is essential to clarify the concept of the exempt amount. Not all fiscal appraisal is subject to taxes. To protect the middle class and lower value housing, the law establishes a large exempt bracket for residential properties, which is readjusted semi annually according to inflation. The territorial tax is calculated mathematically and exclusively on the surplus that exceeds that base exempt amount.

Finally, the tax rates come into play. On the affected amount or surplus, the law applies rates corresponding to fixed annual percentages, which vary depending on whether the property is agricultural or non agricultural. In addition, the regulations contemplate the application of punitive surtaxes, such as those that penalize vacant lots not built within the urban radius, or the recently implemented surtax that levies large real estate assets.

Tax defenses and exemptions: protect your assets

Faced with this powerful state apparatus, the taxpayer is not defenseless. It is imperative to understand that the massive appraisals carried out by the Internal Revenue Service are not infallible and contain very frequent computer and cadastral errors. It is common for the treasury to charge you taxes for a pool that was filled years ago, or to incorrectly classify the material of your house assigning it a luxury it does not possess. In these cases, the law allows filing formal claim resources before the Tax and Customs Courts to demand a reduction in the appraisal and the restitution of undue charges.

In addition to the defense against errors, there are benefits granted by the legislator. The most common legal exemptions include the benefit of law twenty thousand seven hundred and thirty two, which grants substantial reductions and even total exemptions to vulnerable and middle class older adults. Also noteworthy are the historical reductions for properties for exclusively agricultural and forestry use, and the famous tax franchise contained in the DFL two that benefits economical housing with a significant reduction in the territorial tax.

Audit the collection of your property taxes with experts

As we have analyzed, the territorial tax law is an extremely complex framework that intertwines accounting, architectural appraisal, and strict public law. Ignoring how the State values your house and paying blindly can become a silent capital flight, depleting your family savings for years without you realizing it.

At terrenoenregla.cl we understand that your heritage is the result of a lifetime of work. Our interdisciplinary team of tax lawyers and appraiser architects is prepared to audit the fiscal appraisal of your property, detect abusive or improper charges by the Internal Revenue Service, process your legal exemptions, and file legal claims to achieve the definitive reduction of your property taxes.

Need urgent advice?

Click the button above to speak directly with our tax team. Send us the following message for an evaluation:

"Hello Terreno en Regla, I read your technical article about the Territorial Tax Law and I need you to review the fiscal appraisal of my property and my property taxes."